SUMMARY

What’s the easiest way to build wealth over time? Following these everyday savings strategies to help you achieve your short- and long-term financial goals. Here are our favorite savings tools, along with real-life examples you can apply to your own financial life.

Recent events and shifting economic conditions have reminded many individuals to think critically about how to balance short-term financial needs with long-term savings goals. In 2022, roughly 4 in 10 Americans were focused on building an emergency fund, while 31% were working to pay off credit card debt and 27% were focusing on paying for a vacation. Flash forward to 2024 and saving money continues to be a top priority after a turbulent past couple of years. In fact, over 56% of Americans say their top financial goal for 2024 is putting aside money in a rainy-day fund.

Your life stage and individual financial journey can influence which strategies you use to achieve your savings goals. Lynn Carlson, VP Consumer Banking Regional Manager, shares how you can make your money work for you by choosing tools that align with your specific savings goals and timeline. Whether you are early in your career or ready to retire, here are a few everyday savings ideas to consider for your short- and long-term goals:

8 Everyday Savings Tools and Examples

Short-term savings goals

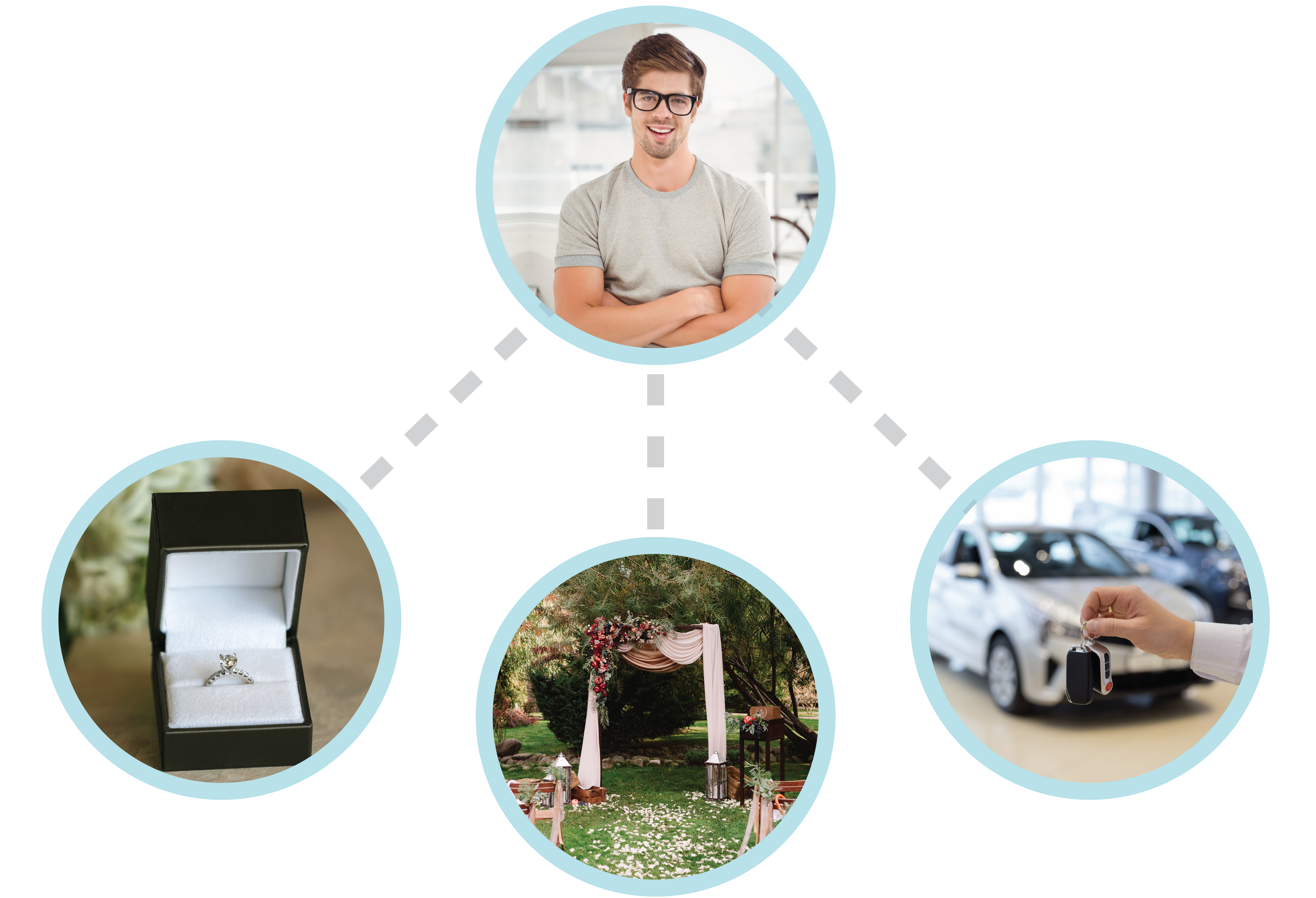

Meet Jared, a recent college graduate who just started his career as a software engineer. He plans to propose to his girlfriend next year and is saving up for the perfect engagement ring. Soon after the engagement, he and his fiancé will plan their wedding – along with the expenses to accompany it. Meanwhile, Jared is looking to purchase a new car within the next three years.

What everyday savings tools should Jared consider? Here are some we suggest:

1. Emergency Fund

Before saving for other goals, most experts recommend setting aside three to six months of living expenses. The emergency fund is intended to cover your day-to-day living costs in the event of unexpected home repairs, medical bills or lost income if you or your spouse were to lose your employment. This money should not be touched except in cases of emergencies.

2. Savings Account

A savings account is the most basic saving option, providing a flexible way for money to grow. Setting up separate savings accounts for different goals can be an effective strategy to jumpstart funds for near-term purchases.

- Grow money with interest: A savings account typically offers more interest than a checking account.

- Easy access: The funds are liquid, meaning you can use or withdraw the money at any time.

3. Money Market Account

A Money Market Account is another liquid savings option suitable for short-term savings goals, particularly your emergency fund.

- Grow your money with interest: A Money Market Account typically offers higher interest than a traditional savings account, allowing more opportunity for money to grow.

- Easy access: Like a savings account, a Money Market Account provides easy access to withdraw funds.

- Other requirements: A Money Market Account typically requires a higher minimum balance than a traditional savings account.

Long-term savings goals

Meet Lisa, a store manager at a local retailer who has worked for 15 years. Lisa and her husband are ready to welcome their third child to the family. They are also planning to buy a vacation home in the next 20 years, shortly before Lisa retires. Meanwhile, Lisa recognizes the importance of saving for retirement along with unexpected medical expenses and her children’s future college education.

In addition to an emergency fund and traditional savings account options, Lisa may consider the following strategies to help her achieve her savings goals:

4. Certificates of Deposit (CD)

A Certificate of Deposit typically has a higher interest rate than a traditional savings account, generally meaning the longer the term, the higher the interest rate and potential return. The main question to ask when considering a CD – or any savings vehicle – is: “What are my plans and when do I need to access this money?” If you are in a financial position to do so, a CD can be a great method to grow your money.

- Flexible terms: You agree to deposit money in the account for an arranged period, with terms generally ranging from three months to five years.

- Grow your money with interest: A CD typically has a higher interest rate than a traditional savings account and is protected by the FDIC, making your money a low-risk investment.

- Less liquidity: A CD is not intended to be a transactional account. The money is less liquid and there are penalties for withdrawing money before the maturity date.

5. CD laddering

CD laddering is a strategy of investing money evenly into several CDs, each with a different maturity date.

6. 401(k) and IRA

There are multiple ways to build your nest egg, depending on your career and the retirement savings plans that are available to you. Among the most common are 401(k) plans, which allow your employer to deduct money automatically from your salary for you to invest. If you do not already contribute to a 401(k), now may be a great time to start, especially if your employer offers a match. Individual Retirement Accounts (IRAs) are available to those who may not have access to an employer-sponsored plan.

7. Health Savings Account (HSA)

A Health Savings Account (HSA) makes managing healthcare costs easier. Account balances can be used to pay for any qualified medical expenses. Contributions are typically tax-deductible, can be spent tax-free and your balances will grow tax-free. An HSA may also be used to pay for out-of-pocket Medicare expenses tax-free in retirement.

8. 529 Plan

Among the most popular college savings plans are 529 accounts to help you prepare for the cost of tuition or college expenses. The money grows tax-free and can be withdrawn tax-free, provided it is used for qualified educational purposes.

Financial planning and your goals

Developing a sound financial plan is essential to achieving your savings goals no matter where you are in life. Healthy savings habits, spending discipline and appropriate investments are all necessary to meet your goals. Aligning your financial plan with your everyday savings strategies and tools can ensure you stay on track to reach your short- and long-term goals.

Let’s start a conversation

Keep in mind there is no one-size-fits-all approach to saving. Everyone’s financial journey looks different, and a financial advisor can help you get where you want to go. Contact one of our experienced advisors to help you assess your savings goals and financial priorities.