Any parent who has gone on a family vacation knows this question. Are we there yet? Most of the time, it is a grating question that is usually answered with “no” and “have some patience”—and rarely the “not far now” that kids want to hear.

As we look for opportunities to change our investment positioning, it can be tempting to ask, “are we there yet?” Of course, the “there yet” portion of the question for our purposes refers to a point when the market and the economy have reflected the recent change in risk.

That is, has the risk of the change in interest rates been reflected? Has the economy slowed enough to approach some sort of equilibrium or inflection point? As a brief background, some time ago we shifted the equity portion of many client portfolios toward less risky stocks—primarily via third-party investment managers—in multiple ways. These included focusing on larger companies and those with healthier balance sheets, more recuring revenue, or other factors of financial “quality,” for a lack of a better term. Managers who focus on these characteristics tend to do better when things are uncertain or there are unforeseen risks in the markets or economy.

PMI helps answer the question

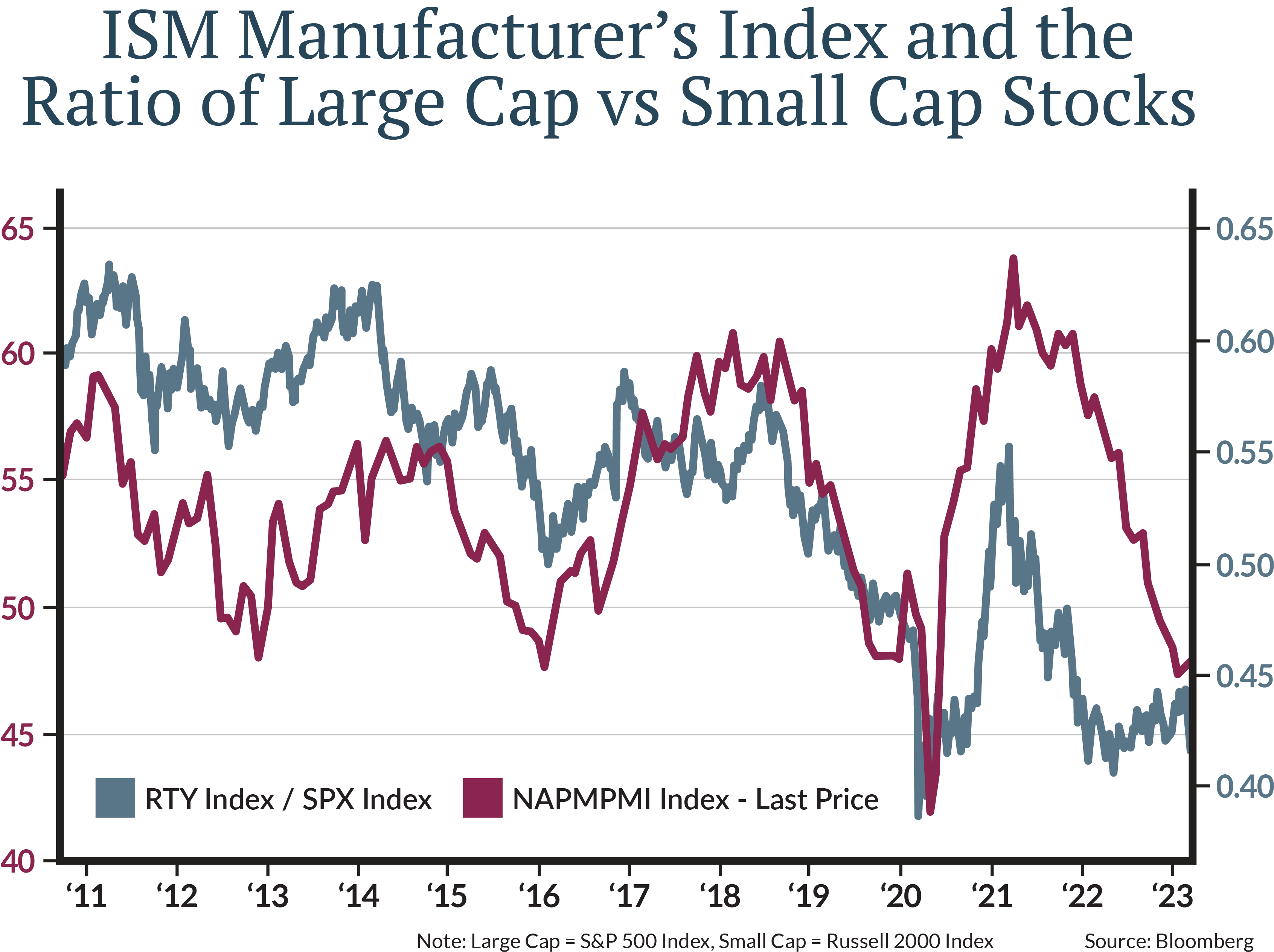

At some point, we will change that positioning and lean back into risk. As we ask “are we there yet,” one thing (among many) we’re watching closely is a measure of the health of the economy called Purchasing Managers Index, or PMI. It indicates the prevailing direction of economic trends in the manufacturing and service sectors. The index summarizes whether market opportunities, as viewed by purchasing managers, are expanding, staying the same, or contracting.

When PMI is trending downward (orange line in the chart below), larger companies have tended to outperform smaller ones (green line). If you look at the recent peak in the PMI during early 2021 until recently it shows large company stocks outperforming small company stocks. The reverse is true when the PMI hits a relative bottom or starts to rise. Those periods tend to coincide with economies recovering from some weak point in the cycle.

So what is PMI telling us about where we are now? It’s the answer the kids in the back seat don’t want—“no” and “have some [more] patience.”

That’s important, because some other indicators are highly positive. For example, companies have plenty of cash, and employment continues to be at a historically strong level. But PMI cautions us against leaning into risk too early. We’ll stay patient and wait for the data to drive the next decision in portfolios.

Keeping on driving forward

In the meantime, we will stick to our existing strategy: keep our relative defensive positioning, rebalance as portfolios get out of balance, and continue waiting out what has been a volatile time for investors.

Just like our family trips, eventually you do get there, but in the meantime, there is a lot we can do to make sure we enjoy the rest of the journey.